If your phone lights up with unknown numbers—and your stomach drops every time—you’re not alone. Debt collection calls can feel relentless, intimidating, and deeply personal. I’ve been there: staring at the screen, wondering if answering will somehow make things worse.

Here’s the good news: you have powerful legal rights, and most collectors are counting on you not knowing them. U.S. law strictly limits how, when, and even if collectors can contact you. Once you understand the rules, the balance of power shifts—fast.

This guide walks you through exactly how to handle debt collection calls legally, what to say, how to stop harassment, and when to escalate if collectors cross the line.

Know Your Rights Under the Law (This Is Everything)

The cornerstone law protecting you is the Fair Debt Collection Practices Act (FDCPA). It applies to third-party debt collectors (not original creditors) and gives you clear, enforceable rights.

What debt collectors cannot do:

- Call before 8 a.m. or after 9 p.m.

- Use threats, profanity, or intimidation

- Call you repeatedly to harass you

- Lie about the amount owed or legal consequences

- Discuss your debt with others (friends, family, coworkers)

According to the Consumer Financial Protection Bureau, harassment includes repeated calls intended to annoy or abuse—even if no one answers.

Saving Queen tip: If calls feel nonstop, start logging them immediately. Dates, times, phone numbers, and voicemails matter.

What to Say When a Debt Collector Calls

You don’t have to explain your life, apologize, or agree to anything on the spot. Keep it short, calm, and strategic.

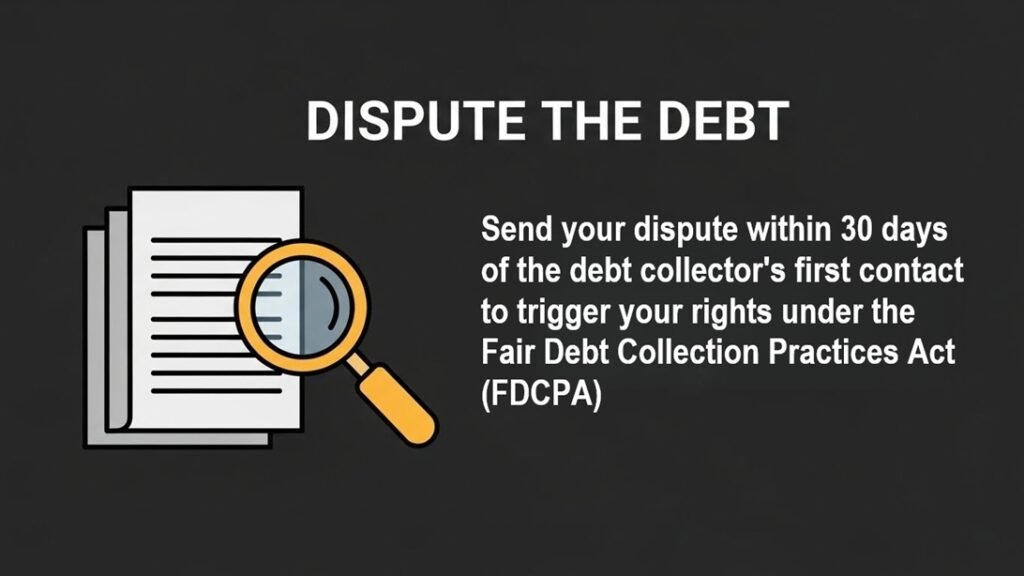

Script #1: Verify the Debt (Your First Move)

“Please send me written verification of this debt.”

Collectors are legally required to provide proof if you request it within 30 days of first contact. Until they do, they must pause collection efforts.

Script #2: Limit Communication

“I’m requesting that all future communication be in writing.”

Once said (and later confirmed in writing), phone calls should stop.

Script #3: If They’re Crossing the Line

“This call is being documented. Please comply with the FDCPA.”

You don’t need to sound aggressive—just informed.

How to Stop Debt Collection Calls Completely

If calls continue, it’s time for the nuclear option: a cease-and-desist letter.

How it works:

- Write a letter stating you want no further contact

- Send it certified mail with return receipt

- Keep a copy for your records

Once received, collectors may only contact you to:

- Confirm they’ll stop, or

- Notify you of specific legal action (rare, but allowed)

Important: This doesn’t erase the debt—it just stops contact. If you’re unsure whether this is right for you, consider speaking with a nonprofit credit counselor.

When Debt Collection Becomes Illegal Harassment

If a collector ignores your requests or violates the law, you can—and should—take action.

Your escalation options:

- File a complaint with the Consumer Financial Protection Bureau

- Contact your state Attorney General

- Speak with a consumer rights attorney (many offer free consultations)

Under the FDCPA, you may be entitled to:

- Up to $1,000 in statutory damages

- Reimbursement of legal fees

- Compensation for emotional distress (in some cases)

Collectors know this—which is why asserting your rights often makes calls stop quickly.

Smart Moves That Protect You Long-Term

✔ Check your credit reports

Some collection calls stem from errors or zombie debt. Pull free reports from AnnualCreditReport.com and dispute inaccuracies.

✔ Never give banking info over the phone

Even legitimate collectors should not pressure you for immediate payment details.

✔ Don’t ignore lawsuits

If you receive official court papers, respond promptly—even if the debt is old or incorrect.

Final Thoughts: You’re Not Powerless Here

Debt collection calls are stressful—but they are not a moral judgment, and they do not mean you’ve failed. They’re a legal process with rules, and once you know those rules, you’re back in control.

💬 Have you dealt with aggressive collectors before? Share your experience in the comments—you never know who you might help.

👉 Want more smart, no-shame money guides? Subscribe to Saving Queen and explore related posts on credit repair, debt relief, and consumer rights.